A decade of the operations of credit reference bureaux in Ghana: a reflection

Financial markets are very fundamental to the economic development of every country. Through the financial intermediation process, scarce financial resources are efficiently allocated to productive sectors of the economy. Surplus funds are channelled from surplus-spending units to deficit-spending units.

Financial markets are very fundamental to the economic development of every country. Through the financial intermediation process, scarce financial resources are efficiently allocated to productive sectors of the economy. Surplus funds are channelled from surplus-spending units to deficit-spending units.

For the financial market to be efficient in performing its role in the economy, it must have the appropriate depth and breadth both on the supply side and the demand side; there must be a broad range of financial products and services to satisfy the diverse needs of various customers. Large businesses, small and medium enterprises (SMEs), retail businesses as well as individual economic units need access to varying forms of both short-term and long-term financing to expand their businesses. Also, efficient and proper functioning financial markets imply operational, informational and allocation efficiencies.

Operational efficiency exists when financial transactions or service costs are reduced to the barest minimum. Thus, investors are able to pay the lowest fees to earn a decent profit. Informational efficiency implies that, the prices of financial market instruments properly reflect all available information. Allocation efficiency is when capital is channelled and distributed to its very best use. Financial market participants are able to use accurate and available market information to make informed decision about how to allocate financial resources. Therefore, financial institutions thrive on the existence of reliable information to channel capital to the sectors of the economy where they can be put to best use.

Both financial and economic literature contend that one of the sources of market failure is information asymmetry—when parties of an economic relationship have unequal level of information. In markets where one party has superior knowledge of a relationship than others, it may lead to adverse selection and moral hazard problems. This could result in mistrust and eventual discontinuity of vital financial services. Thus, to curb these problems, certain institutions have sprung up to facilitate financial transactions by providing reliable information in the financial markets. One key institution of this sort is the credit rating or credit referencing agency. Their existence is very critical for financial market development in any economy. Credit reference agencies provide avenues for the independent assessment of firms’ or individuals’ credit quality.

Credit reference bureaux (CRBs) facilitate credit information sharing among financial institutions. Such agencies are able to use verifiable information to thoroughly assess a unit’s borrowing history, repayment characteristics and cash flow position among others. This vital information is used to form an opinion or predict the current and future credit worthiness of individuals and entities. It is very obvious that, the free flow of reliable and credible information ensures transparency and fairness which are very critical for the development of financial markets.

In line with this, the Bank of Ghana enacted the Credit Reporting Act, 2007 (Act 726) in the latter part of 2007 which eventually paved way for the operation of credit reference bureaux in Ghana. Consequently, XDS Data credit referencing bureau fully commenced operations in 2010 as Ghana’s first credit referencing bureau. Along the line, two others, Hudson Price Credit Bureau and Dun and Bradstreet Credit Bureau Limited also began operations in the country.

Have they lived up to expectation?

Given that the presence of well-functioning credit referencing bureaux reduces asymmetric information and its associated problems in financial markets, improvements in the credit delivery, easy access to credit and reduction in bank’s non-performing loans following the advent of CRBs in Ghana should be expected. The presence of CRBs in the financial market presents a win-win situation for financial institutions on one hand and borrowers on the other hand. Financial institutions get credit information on prospective borrowers that can facilitate processing of credit requests to reduce the risks of bad debts. On the borrower’s side, a good credit record provides an incentive for competitive pricing of loan facilities. Several studies have shown that credit reference bureaux reduce borrowing costs and bad loans to some extent.

In the Ghanaian context, several concerns need to be addressed after years into their operations. Questions pertaining to visibility of their operations, how efficient they have been, the extent to which their services are used by the banks and how their activities are reducing credit risks are yet to be answered. The limited use of their services stem from several factors such as poor visibility of their activities, cost implications among others.

Currently, some of the reference bureaux have separate data on borrowers, a reason some financial institutions are recalcitrant in patronising their services. A financial institution may sign on with one of the bureaux alright but that bureau may not have data on some borrowers who may approach that institution for a facility. So, for a financial institution to leverage the full benefits of these bureaux, that institution must sign on with all the bureaux operating in Ghana. However, these services are offered at a cost. Thus, the huge cost implication may deter some financial institutions especially the Micro-Credit institutions with less financial muscles.

Also, regarding the number of financial institutions that are subscribing to their services, studies have shown that some of the financial institutions are very reluctant to engage in information sharing with the credit referencing bureaux for fear of their major customers being poached by other financial institutions. Not only does this development affect the operations of the credit reference bureaux, it also reduces the pool of credible information at their disposal from which other financial institutions can tap. Thus, this lackadaisical attitude of some financial institutions to share information with the credit referencing agencies may deepen the already existing information asymmetry problem.

Access to credit facility remains a major problem especially among the small and medium enterprises (SMEs), retail businesses and individuals despite the operation of credit reference bureaux. This contradicts the general notion that the existence of credit referencing bureaux improves access to credit. Over 80 per cent of Ghanaian businesses are in the informal sector where poor business record keeping is prevalent. This to some extent explains why access to credit by SMEs and retail businesses are very difficult. Besides they are also not aware of the activities of these credit reference bureaux which they can utilize to improve their access to credit and reduce their borrowing cost.

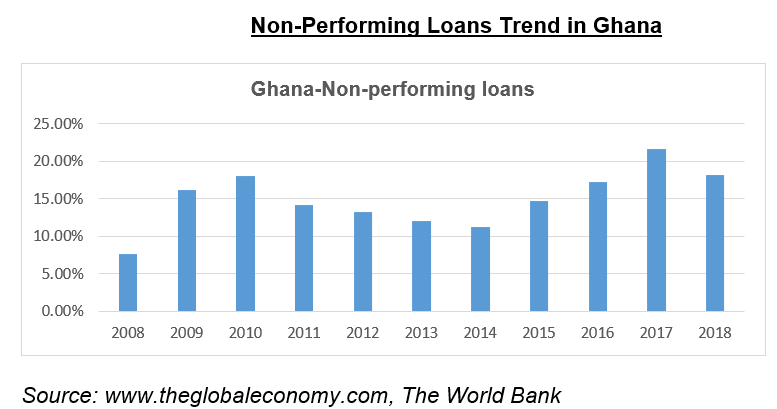

Non-performing loans in the banking sector has witnessed some interesting trends following the commencement of the activities of credit reference bureaux in Ghana. All other things being held constant, it can be observed from the graph that prior to the activities of credit reference bureaux in Ghana in 2010, non-performing loans were increasing unabatedly. Following the commencement of their operations, non-performing loans decreased yearly till 2014. These initial gains were reversed from 2015 to 2017 before falling in 2018. Though the rise in non-performing loans in 2017 can be partly ascribed to the banking sector cleansing which led to the revocation of the operating licences of some banks, it can be inferred that the activities of the credit reference bureaux are partly having significant positive impact on the non-performing loans in the financial sector.

What is the way forward?

What is the way forward?

The presence of credit referencing bureaux in Ghana is gradually having impact on financial market development through the improvement in credit delivery. Nevertheless, their activities are fraught with a number of limitations which need to be addressed as a matter of urgency so that they can fully perform their role in reducing information asymmetry for better financial market development.

Firstly, Bank of Ghana should fully enforce the provisions of the Credit Reporting Act 2007, (Act 726) which paved way for the operation of credit reference bureaux. Financial institutions should be mandated to share information on the credit history of their borrowers to the credit reference agencies. Violators in this regard should be made to face the full rigours of the law.

Financial institutions should be admonished to embrace the bigger picture and stop harbouring the fear that they can lose their major customers to competitive financial institutions.

The passage of the Data Protection Act, 2012 (Act 843) is meant to protect the privacy and personal data of individuals. Non-compliance with the provisions of the Act is an offence which may attract civil liability or criminal sanctions or both depending on the magnitude of the infraction.

Thus, being guided by this act, credit reference bureaus therefore cannot be disclosing private and confidential information about customers except disclosure within their mandate as prescribed by law.

Financial institutions should therefore be rest assured that information sharing with the credit referencing bureaux will allure to their ultimate benefit.

In a hypothetical example, let’s assume that customer A goes to borrow from Bank X and goes to Bank Y for another credit. These two institutions share the credit history with the credit reference agencies. Customer A again goes to Bank Z for another loan request, should Bank Z resort to the credit reference bureau for information on customer A, quickly they will know the credit history and base on that, Bank Z can reduce its single obligor limit to customer A. This would not put undue pressure on customer A who is already saddled with loans from the other two banks. The overall effect is that customer A can honour his or her payment obligation to all the banks which will reduce the possibility of the loans going bad with these institutions.

Secondly, public education should be intensified on the importance of credit referencing bureaus in the development of financial markets.

Financial institutions and borrowers should be encouraged to use their services. This will reduce lending premiums and reward borrowers of good credit quality with good lending rates whiles bad borrowers in the financial market are also exposed. Also, the credit reference bureaus should be empowered to source information about businesses and individuals independent of the ones provided to them by the financial institutions. This will enable them to have a comprehensive view of potential customers and better assess their credit worthiness. Also, this will enable them to have information on businesses and individuals with no borrowing history to better assess them during their first credit request from the financial institutions.

Conclusion

Credit reference bureaux play a vital role in financial market development by mitigating asymmetric information and its associated problems in financial markets. This facilitates efficient allocation of capital to the productive sectors of the economy. Thus, their activities should be given the much-needed attention to better leverage on the numerous benefits they present for financial market development.

By Daniel Taylor & Bernard Sarpong

Emails: [email protected]; [email protected]